Business payments in Canada: a trilogy of surveys point to inefficiencies

DISCLAIMER: Articles are written to reflect the interests and views of the author(s), and are not intended as an official Payments Canada statement or position.

Summary

The global payments landscape continues to evolve in line with the commercial demands of businesses and their stakeholders. While resources devoted to payments processing by Canadian businesses are estimated to have declined proportionally in recent decades, survey evidence points to remaining cost inefficiencies. This essay discusses common findings from three recent surveys on business payments processing in Canada, all of which point to lingering inefficiencies and businesses’ desire for change. Payments Canada’s Modernization initiative – notably fostering adoption of the ISO 20022 payment messaging standard, coupled with expedited payments processing – is expected to help address these remaining inefficiencies. For these benefits to accrue, education and awareness among Canadian businesses and their stakeholders of available payments processing options and their relative merits in a modernized environment is critical. Put differently, Payments Canada’s Modernization initiative should not be viewed as an end-point, but rather as a launch pad for enhanced payments processing efficiency in Canada.

In an age of near ubiquitous Internet access and smartphone ownership, global commerce continues to evolve as businesses strive to offer a seamless customer experience across a range of channels. Business operations are becoming more complex as a result, which can often require close coordination of sales, treasury and accounting functions, as well as managing relationships with customers, suppliers, financial intermediaries and service providers, across geographies.

The global payments landscape has undergone material change in line with this evolution. Payments ecosystems around the world – including here in Canada – continue to develop with new players, partnerships, and products being brought to market. There is growing awareness of the importance of fostering innovation and competition in this space to help underpin economic growth, while still preserving the safe and secure payments environment that users expect and deserve.2

These developments have prompted increased use of electronic payment methods by Canadian businesses and consumers over time, largely as a substitute for legacy payment methods such as cheques which entail a higher social cost from a processing standpoint (Wells 1996; Arjani 2015). In today’s competitive landscape, Canadian businesses understand that investing in improvements to their payments processing practices can lead to greater customer satisfaction, lower costs, and new revenue opportunities.

This essay is intended to support this cause by highlighting recent survey evidence of lingering inefficiencies in business payments processing. What is interesting, and perhaps reassuring, is that three recent survey studies conducted independently and leveraging diverse methodologies produce similar findings, which suggests an underlying theme in the business payments processing space in Canada. The essay explains these findings in some depth with the hope of generating dialogue among businesses and service providers on how Payments Canada’s Modernization initiative could support improved outcomes.

How Canadian businesses transact today

Today, Canadian businesses transact with their customers and suppliers using a range of electronic payment options, including wire, pre-authorized debit, direct credit, credit and debit card, and Interac e-Transfer, to name a few. Indeed, Tompkins et al (2015) provide compelling evidence of the role of direct credits and pre-authorized debits in displacing cheques in Canada over the past two decades. Payments service providers too are looking beyond just payment methods, offering a host of value-add services to help their business clients succeed.3 For example, Square helps make card acceptance viable for businesses of different sizes and service models while supporting straight-through-reconciliation and business analytics from the same platform. PayPal appeals to online merchants via delivery of sophisticated global payment and online invoicing solutions. Interac’s recent launch of its Request Payment, Autodeposit and Bulk Disbursement services has also been popular among businesses, as a complement to the Interac e-Transfer platform. As well, the web-based banking portals for small and medium-sized businesses (SMBs) offered by Canada’s largest financial institutions look quite different today than even five years ago, with new services and improved functionality to support business decision-making. The recently announced collaboration between Royal Bank of Canada (RBC) and Canadian FinTech player Wave to enhance RBC’s online business banking platform is but one example here. Payments service providers are both competing and collaborating to meet the increasingly complex needs of Canadian businesses.

Inefficiencies remain largely due to reliance on legacy payment instruments

Despite these developments, there is still evidence of cost inefficiencies in business payments processing in Canada. To learn about the nature of payments processing costs and the pain points faced by Canadian businesses in achieving further efficiencies, Payments Canada has been working with market surveillance partners to engage businesses directly through a number of survey studies.4 While the methods and samples differ across these studies, their findings are generally consistent, and they affirm several aspects of Payments Canada’s Modernization initiative. Perhaps most notably, the survey results support adoption of the ISO 20022 payment messaging standard in Canada and related engagement with enterprise resource planning (ERP) systems providers to foster straight-through-processing and reconciliation. The findings also support efforts to improve the transparency and timeliness of funds availability for payees. Importantly as well, the studies suggest that Payments Canada’s Modernization initiative should not be viewed as an end-point. Instead, improvements underway to core clearing and settlement systems are expected to promote further innovation and product development by payment service providers which, in turn, could motivate behavioural change among consumers and businesses to derive full benefit from the changing environment.

The remainder of this essay goes deeper into these findings and looks forward to the prospective benefits of payments modernization in Canada.

The EY (2018) study highlights five potential factors that contribute to higher than necessary payments processing costs for Canadian businesses. First, the current inability for full remittance information to travel with most forms of electronic payment results in reduced opportunity for automated matching of payments to invoices.5 This limits the potential for straight-through-processing, instead requiring costly manual efforts to perform reconciliation. The EY (2018) study indicates an auto-match rate of 75 per cent across different industries in Canada, suggesting that improvement is possible on this margin with associated cost benefits. Moreover, it finds that low auto-match rates are particularly evident in industries with a high prevalence of off-invoice early payment discounts, volume- or rate-driven deductions, allowances, rebates and commissions. The opportunity for richer remittance data presented by the ISO 20022 payment message standard could help support straight-through-processing for these more complex use cases.

Second, lack of remittance information traveling with a payment can also lead to shortcomings in supporting effective supply chain management. Such limited information can also impact collections efficiency as manual effort is needed to address delinquent payments and any reconciliation discrepancies.

Third, inconsistency in the timing of payment receipt across payment instruments – and even differences in timing for the same instrument (e.g., EFT) depending on whether a payment clears over accounts at the same financial institution or clears over accounts at two different financial institutions – can create unwanted variance in cash flow forecasting accuracy, thereby reducing predictability in short-term cash requirements for businesses. Delays in payment receipt can also lead to increased days sales outstanding and to more cash tied up in accounts receivable, which increases working capital costs. Feedback from study participants indicates that expedited payments processing could help avoid one to three days of borrowing in this context.

Fourth, several areas for improvement in cross-border payments were flagged by respondents, including better traceability of payments, more transparent pricing, higher predictability of payment timeliness, and improved integration across jurisdictions on standards, technology, rules and procedures governing payment exchange, clearing and settlement. Finally, the EY (2018) study points to the benefits of further investments in technology and automation to help streamline payments efforts. Examples include investments in cash application software, ERP configuration and design, treasury management solutions, and outsourcing to specialist providers.

According to EY (2018), aggregate payments processing costs for Canadian businesses are estimated between $3 billion and $6.5 billion each year, where some portion of these costs is being driven by the factors mentioned above and could be reduced in a modernized environment characterized by ISO 20022 capability and expedited payments processing. While one could perhaps debate the assumptions and modeling approach used to derive these figures, and what proportion of total costs might represent “inefficiency”, it seems reasonable to conclude that payments processing costs are generally material for Canadian businesses, with room for improvement.

The EY (2018) findings indicating scope for payments cost reduction are consistent with those from the Leger (2018) and RFi Group (2018) studies, and also with earlier studies of the business payments landscape in Canada (e.g., CFERC 2011). For example, over half of businesses surveyed by Leger (2018) believe they spend too much time on payment processing activities, including tracking payments and matching payments to invoices. Moreover, 87 per cent of Leger (2018) respondents believe it is important that the payments industry continues to evolve and offer services that streamline the processing and reconciliation of payments in Canada. Earlier studies by Tompkins et al (2015), Arjani (2015) and CFERC (2011) indicate that current shortcomings in electronic payment methods (e.g., challenges in automated matching of payment to invoice) drive businesses to continue to rely on more socially-costly methods of payment, including cheque and cash, despite a general willingness to move away from these methods if a viable alternative were to emerge. Indeed, roughly two-thirds of the nearly 900 million cheques written in Canada each year can be attributed to businesses (Tompkins and Galociova 2017). The RFi Group (2018) survey confirms that SMBs remain heavy users of cheques in Canada, with 59 per cent of SMBs indicating use of cheques to pay for expenses. This survey finds that roughly a fifth of total business expenditures of SMBs are paid by cheque, with the most-cited cases being rent, government payments/taxes, and payroll. Cheques and cash remain the most common payment methods accepted by Canadian SMBs by a wide margin in the RFi Group survey.

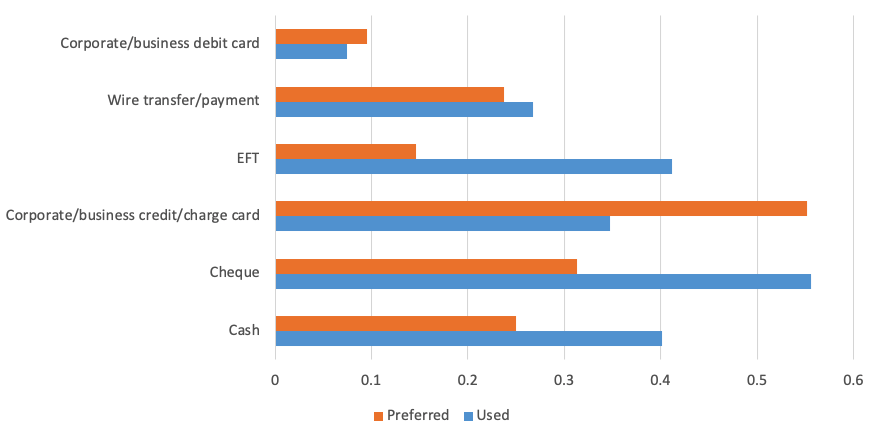

A further finding from these surveys is the suggested misalignment between how Canadian businesses say they prefer to send and receive payments, and how they actually do so. For example, the Leger (2018) survey points to higher than preferred prevalence of cheque and cash in receiving payments from customers among SMBs, and lower than preferred use of certain electronic methods – particularly Interac e-Transfer – to pay suppliers and vendors. Moreover, the Leger (2018) survey finds that 69 per cent of businesses currently accepting and writing cheques would be willing to move away from them if a more convenient electronic method were available. Similar findings come from the RFi Group (2018) survey, where 56 per cent of SMEs and corporates indicated using cheques to pay for business expenses during the survey period.

Notably, 31 per cent of businesses say that cheques would remain a preferred method to pay for expenses were all options open to them – a differential of 25 per cent !

55 per cent of businesses also stated that they would prefer to use much more corporate/business credit cards (in terms of use, this number was only 35 per cent). Figure 1 below offers an overview of preferred versus used payment methods.

Figure 16: Used versus Preferred Payment Methods7

Barriers to greater adoption of electronic payment methods

With the number of electronic payment options available to businesses today, what precludes them from advancing use and acceptance of these methods? The surveys offer evidence here as well.

- Deficiency of attractive electronic payment options: As mentioned, Canadian businesses’ continued reliance on cheques has much to do with a view that electronic payment options do not currently support straight-through-processing and reconciliation and this limits the business case for conversion to electronic. This likely also underpins the finding above from the Leger (2018) survey that, while 69 per cent of businesses that accept and use cheques would be willing to move away from them if a viable electronic alternative existed, about half of respondents still cite cheques as a preferred way to send and receive payments. Introduction of the ISO 20022 payment message standard carries many anticipated benefits, but perhaps most importantly in this context is that it should foster straight-through-processing and reconciliation for businesses in Canada as more information (both content and type) will be able to travel with a payment under this standard. Moreover, other pending changes as part of Payments Canada’s Modernization program, including an additional daily file exchange and more timely funds availability to recipients for direct credit transfers and pre-authorized debits, should also enhance the appeal of electronic payment methods for Canadian businesses. These enhancements will replicate the benefits that businesses see with cheques today, enabling them to move away from cheques even more rapidly without compromising service levels.

- Suppliers and customers also need to adjust behaviour: In the earlier CFERF (2011) study, 39 per cent of respondents identified customer habits and behaviours as a barrier to increasing adoption of electronic payments (this was the top mentioned barrier), while 34 per cent also indicated that it was difficult to motivate suppliers to accept electronic payments. Seven years later, a similar message was conveyed in the Leger (2018) survey, where 50 per cent of respondents indicate that customers influence their decision to accept new payment methods, and another 29 per cent indicate that suppliers influence their decision to adopt new payment methods. Importantly, customers and suppliers were the top influencers cited by respondents in this study. There are various anecdotes attempting to explain these results. For instance, suppliers may be unwilling to provide bank account information out of concern for safety and security, and instead prefer to accept a cheque for payment instead. Another is that customers may prefer to use cheques (and credit cards) in favour of more immediate electronic payment methods such as Interac e-Transfer because the former offers more flexibility from a cash management perspective, e.g., continuing to have access to funds between when the cheque is delivered to the payee and when funds are actually deducted from their account. This may also be in line with another anecdote we have heard about customers feeling more ‘in control’ of the payment when they pay by cheque. Alternatively, some businesses may simply prefer to rely on their physical chequebook as a record-keeping device.

For some consumers and suppliers, preference for cheque payments is based purely on habit, or perhaps due to lack of knowledge of potential electronic options. For instance, stories abound of rental tenants wishing to pay their landlord by Interac e-Transfer instead of cheque, or a parent wishing to pay for their child’s school activities using Interac e-Transfer instead of cheque, but where both are unable to do so because the landlord or school only accepts the latter. There may also be a perception that cheques are a cheaper or safer means of payment compared to electronic; however, it is important that one takes into account the full cost of cheque issuance including fraud and security risk and other operational risks related to cheque processing in their evaluation. While developments like remote deposit capture (RDC) and Payments Canada’s Image Rule Project may reduce the overall costs of cheque processing at the margin, they do not eliminate operational risk, e.g., challenges with duplicate deposits of the same cheque using RDC. - Concerns regarding safety and security: For customers and businesses alike, safety and security are paramount in the choice to adopt a new payment method. This was evident in the Leger (2018) survey, where “safety and security” was ranked as the top payment priority for respondents (49 per cent of the time) – ahead of “lower transaction fees” (34 per cent) and “faster payments processing” (14 per cent). With all the news of corporate data security breaches, perhaps some users are apprehensive to shift to electronic options and would rather pay using cash or cheque. However, this would seem peculiar given that one’s bank account information is provided at the bottom of each cheque. Notwithstanding, an increasing number of Canadian businesses have embraced credit card as a preferred means of payment in recent years (Tompkins and Galociova 2017), suggesting they continue to see this method of payment as a safe and secure option.8

All of the reasons mentioned above suggest that education and awareness of the characteristics and relative merits of different payment options by use case, and of the core tenets of payments system modernization, are central to maximizing the economy-wide gains from this initiative. And there is reason to be optimistic – from the Leger study, 81 per cent of SMBs indicate that they are willing to invest and integrate new technologies into their operations if it presents opportunity for enhanced profitability.

Concluding remarks

There have been many positive developments in the business payments landscape in Canada in recent years.

Payments services providers – both new entrants and incumbents – are working continuously to bring new payments processing services and functionality to businesses to help strengthen the bottom line.

Yet there is evidence that cost inefficiencies remain in this area, which could be addressed by Payments Canada’s Modernization initiative and in collaboration with payments services providers. For this to materialize, businesses’ education and awareness of current and prospective products and services and their relative merits in meeting user needs is critical.

How best to ensure that this education and awareness materializes? What do you think about the current and future prospects for business payments processing in Canada? We welcome and encourage readers to continue the dialogue in the comments below or to reach out to the authors directly.9

The Authors

Viktoria Galociova

Viktoria Galociova

As an Economist at Payments Canada, Viktoria is the lead author and researcher working on Payments Canada’s annual flagship publication: the Canadian Payment Methods and Trends report. Viktoria is also in charge of supporting the Modernization team, the Research team’s external blog and annual conference, as well as evaluating alternative data service options for the organization including supporting and contributing to the ecosystem surveillance function. Viktoria is also an active member of the Payments Canada Strategic Foresight Team. Viktoria’s recent work includes research on Canadian and international payment industry trends and international retail payment system research. Prior to joining Payments Canada, Viktoria conducted research relating to the economic impacts of oil prices, returns to higher education, the impact of socioeconomic factors on labour market outcomes and the impact of oil prices on housing markets. Viktoria holds a Master’s Degree in Financial Economics and a Bachelor’s Degree in Economics and Business from Carleton University.

Neville Arjani

Neville Arjani

Neville Arjani serves as Director, Research at Payments Canada. He and his team are responsible for delivering thought leadership, analysis and advice to support the strategic and operational priorities of the organization. His research interests include settlement risk management in clearing and settlement systems, intraday liquidity management, technology and payments, and the contribution of payments systems to broader economic and financial outcomes. Neville joined Payments Canada in 2014, following nearly five years in a research and policy capacity with the Office of the Superintendent of Financial Institutions (OSFI) and nearly eight years in a similar capacity with the Bank of Canada.

1 The views presented in this paper are those of the authors and do not necessarily reflect the views of Payments Canada.

2 For example, Humphrey et al (2001) and Humphrey (2003) represents seminal work exploring the economic benefits of payments innovation.

3 In this note, the term payments service provider is broad in scope, and includes any organization involved in helping businesses send, receive, and process their payments.

4 Focus is on results from three recent surveys. These include Ernst and Young’s study entitled How can payments modernization benefit Canadian businesses? (EY 2018), Leger Marketing/Payments Canada’s Payments Pulse Survey (Leger 2018), and results from RFi Group’s Canada SME Banking and Payments Council and Canada Commercial Banking and Payments Council (RFi Group 2018).

5 In contrast, a copy of the invoice and other details of payment can always be mailed together with a paper cheque in an envelope to the payee.

6 RFi Group’s Canada SME Banking and Payments Council and Canada Commercial Banking and Payments Council (RFi Group 2018).

7 This figure includes both SMEs and corporates. Questions asked: “How does the business pay for the following expenses” and “Which method of payment would the business most prefer to use for the following expenses?”.

8 This may also be due to the fact that, in some cases, the issuer of the credit card may be willing to assume liability in the event of unauthorized card use.

9 The authors’ contact information can be found in their respective bios.