Is Canada moving towards a cashless society?

DISCLAIMER: Articles are written to reflect the interests and views of the author(s), and are not intended as an official Payments Canada statement or position.

Summary

Recently, we have seen significant discussions in payments literature regarding countries moving towards becoming cashless societies. In Canada, electronic payment alternatives to the use of cash have flourished, in the form of credit and debit cards with merchants, a variety of electronic payment instruments options for conducting e-Commerce and the use of INTERAC e-Transfers for P2P payments. Despite the progress made with electronic payments, cash volumes remain relatively high in Canada. In this article, we focus on the heavy users of consumer cash payments in Canada, to better understand the main areas where electronic payments are coming up short in providing alternatives to the use of cash. Our market research suggests that cash is still prevalent and will continue to be an important medium of exchange unless some difficult challenges are addressed. Further innovation is required to better serve rural, lower income, underbanked, and older Canadians to ensure viable alternatives to cash exist for all Canadians. Finally, we examine Canadians who use digital currencies. In Canada, digital currencies are serving mostly only the affluent and those well placed for capitalizing on traditional financial institution relationships and payment methods.

In this article, we discuss whether or not Canada is truly moving towards a cashless society. We do this by first focusing on cash and electronic payments separately and then bringing the findings together. In 2018, Payments Canada launched a customized survey on consumers’ payment habits in Canada.1 Conducted on a quarterly basis, Payments Canada receives insights on 7,500 Canadians every year, resulting in 525,000 data points. As a major contribution to the Canadian Payments Methods and Trends research, the primary objective is to provide a holistic view of the payments market.2 Our sample is representative of the Canadian population, taking into account population representation across the Canadian provinces.3

Alternatives to cash found in electronic payments

Electronic methods of payment have been growing significantly in the last decade in Canada. More Canadians are starting to appreciate the benefits of using electronic payment methods such as credit and debit cards for their everyday purchases. With almost 90 per cent of Canadians owning both a debit and a credit card, we can see that electronic payments are highly entrenched into the payment habits of Canadians across all age groups. However, we do still find some differences, with younger Canadians using new channels, such as mobile contactless, on a more frequent basis. As we will discuss throughout this paper, cash continues to be a part of Canadians’ everyday purchases but, at the same time, it is being challenged by the more convenient electronic options.

Although payment habits do not change overnight, we continue to see significant changes year-over-year. Could this be the beginning of a new era for electronic payments? Or will more traditional payment instruments still hold their ground? Is it true that Canada is moving towards a cashless society? In the sections below, we analyze cash and electronic payment usage of Canadian consumers and discuss this broader question.

Credit and debit cards - who is the front runner?

Credit cards are very popular among Canadians, especially for higher value payment items. To compare, our data show that debit cards are used, on average, the same number of times per week (seven times) as credit cards, but the average value of credit cards is double that of debit cards. Our analysis indicates that this is associated with the benefits users reap from rewards cards. About 80 per cent of respondents have a credit card that offers some form of reward, with cashback rewards being the most popular, especially in Quebec. Another reason for the higher use of credit cards is linked to its convenience and ubiquity but also the opportunity to consolidate payments into one single bill payment. On average, Canadians spend approximately $1,500 per month and we find that younger and less affluent Canadians are more likely to carry a balance. However, our data also show that older Canadians tend to owe more money, compared to younger Canadians. Residents in British Columbia and Alberta were found to spend more using their credit cards compared to the other provinces. However, Canadians living in the Prairies and Atlantic Canada were found to be significantly less likely to have used their credit card, which may be associated with the higher paper-based payment usage in these regions. The data show that debit cards are used more frequently by younger and less affluent Canadians, while we see the opposite when it comes to credit cards - indicating that money management is a major reason for steering away from credit cards for younger Canadians.

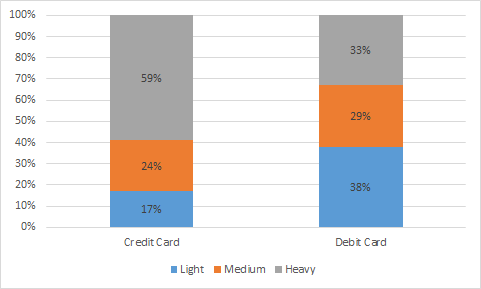

One important factor to consider when analyzing the usage of payment methods is to look at the heavy usage, which indicates a clear preference of a specific payment method over another. Figure 1, below, illustrates that almost 60 per cent of respondents consider themselves heavy credit card users, while only 33 per cent of respondents indicated they are heavy debit card users. The majority of the heavy credit card users are aged 55 and above (at 43 per cent). Heavy debit card users, on the other hand, tend to be between 25 and 44 (at 35 per cent).

Figure 1: Heavy credit and debit card users4

Note: The percentages are based on a respondent's monthly spend in terms of value

Contactless payments are also gaining a lot of traction in Canada, due to their convenience and simplicity of use. Contactless has been increasing significantly in the last couple of years, providing for a great alternative to cash. Overall, about two-thirds of Canadians indicated having used contactless with their credit cards, spending, on average, $320 in the last week. Once again, we see a similar trend on the debit side, with 50 per cent of Canadians using contactless debit but spending about half of what they do using their credit cards. Our data show that younger, higher earning Canadians and those located in British Columbia and Ontario were significantly more likely to have tapped their credit cards. This payment method has become a popular substitute for lower value cash usage at the POS. Mobile contactless usage for credit and debit is quite similar (one-third) indicating that we may see some shifts away from credit cards as new channels (such as Apple Pay and Samsung Pay) become more prominent. This fairly new payment instrument is mostly popular among younger Canadians. In terms of both contactless and mobile contactless, Quebecers were least likely to have tapped their cards compared to the other provinces.

Online transfers paving the way for P2P payments

Online transfers are becoming the go-to choice for Canadians for person-to-person (P2P) purchases, providing a quick and easy substitute for cash or cheques. Our survey data show that almost half of our sample has used this service, with an average of four transactions worth $606 per month, and it is most popular among younger Canadians. About 70 per cent of our respondents use INTERAC e-Transfer to pay their family members, friends and/or acquaintances and almost half have used it to pay a bill or pay a business. Many Canadians make use of this service for their rent payments and we find that younger and lower earning Canadians made more INTERAC e-Transfer payments to a business or to pay a bill, while younger and higher earning Canadians were more likely to have made an INTERAC e-Transfer to a person. Respondents from Quebec were significantly less likely to have made an INTERAC e-Transfer payment to a person, compared to the other provinces, indicating a significant opportunity for enhancing electronic payment services and options in Quebec.

Our survey indicates that PayPal is another online transfer service that continues to grow. Over half of the survey respondents reported that they have a PayPal account, with about four out of ten accounts being used at least once last month. The data suggests that PayPal was used most often by those between the ages of 25 to 44 and those with higher earnings. PayPal only makes up a small share of overall value of e-Commerce and our respondents indicate that about 45 per cent of PayPal transactions are linked to credit cards, providing another convenient means to initiate credit card payments online.

e-Commerce - the flourishing power of online payments

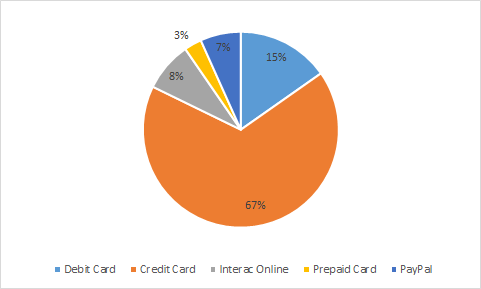

Making online purchases has been yet another very important channel for consumers to use with the convenience of sitting behind their laptop or mobile phone at the comfort of their homes. People can now access virtually any store in the world (as long as the store is set up online), providing a whole new level of globalization. The point-of-sale (POS) is no longer brick and mortar dominated. In Canada, online commerce or e-Commerce happens about five times a month, with an average spend of $340, mobile phones or tablets being the most popular to make purchases. Overall, we see a high inclination towards credit cards in this space where over half of consumers use their credit cards to make online purchases (spending, on average, $446). Once again, we see debit cards in second place averaging about half the value of credit cards but, interestingly, having a higher number of transactions (nine versus six transactions for credit cards). Over half of the debit cards in our analysis are co-badged (with Visa or Mastercard), especially among young Canadians and Ontarians, providing an easy option to pay for purchases online. Figure 2, below, illustrates the dominance of credit cards in this space, making up about 67 per cent of the total payment value shares in e-Commerce.

Figure 2: e-Commerce payment value shares

In-app purchases are providing yet another convenient channel for making payments. Among those using in-app purchases, Starbucks and Tim Hortons rank number one with their mobile application and the option to order ahead and we see many other competitors following suit. Canadians make, on average, about four in-app purchases per month. This trend is most common with younger consumers, making the highest number of not only in-app purchases but overall online commerce as well.

Cash - a dethroned king?

Cash payments have been steadily declining since 2011, when contactless credit and debit cards gained popularity. Despite the convenience of contactless cards, cash still maintained a significant portion of the monthly spend in terms of volume and value. In the past, many articles claimed cash is king in Canada, but is this still the case in 2019?

Due to the anonymity of cash transactions, it is also difficult to capture the exact usage of cash. Despite these challenges, the cash section of our consumer survey aims to obtain a snapshot of consumer cash usage in Canada. We asked respondents about their cash usage in the last seven days in terms of volume and value. We then created sub categories of cash users into light, medium, and heavy cash users.5 We also investigate cash usage in terms of banking status and demographic factors.

According to the consumer survey results, 81 per cent of respondents indicated they have used cash in the last week. In terms of the total volume and value of popular payment instruments (cash, debit card, credit card, and cheque), cash accounted for 16 per cent of the total monthly value6, and 26 per cent of monthly transaction volume, which shows that cash still accounts for a significant portion of the market share. Different results and use cases arise when looking at cash payments made to a person or a business. Roughly 80 per cent of Canadians used cash to pay a business in the last seven days, averaging two transactions per week, and $169.7 Of all the cash users, 45 per cent of the respondents indicated they have given cash to people (friends and family) in the past seven days, averaging four transactions per respondent and $157. In a follow-up question, we surveyed why people choose to use cash, and found that when people use cash one of the main reasons is “person would only accept cash”. This indicates that when it comes to P2P payments, consumers would prefer to pay using other options (such as, for example, INTERAC e-Transfer), but are unable to given preferences of the recipient. We see a similar story on the cheque side as well where 34 per cent of people from Quebec who use cheques to pay for rent (this is the province with the highest cheque usage) indicated that there are no other payment options given to them, which shows that the lack of alternative payment methods when it comes to paying for rent may be the primary reason why people are still using cheques.

Who is driving heavy cash usage in Canada?

Fifteen per cent of Canadian consumers are considered heavy cash users and they tend to be younger, from Manitoba or New Brunswick and with an income of less than $19,000 per year. We also find that about one in four of these younger Canadians do not own a debit or a credit card, which may be contributing to their higher-than-average cash usage.

Another important segment of the population who needs to be taken into consideration when looking at cash usage are the unbanked consumers.8 We define the unbanked as those individuals who do not have a credit or a debit card. Cash usage in terms of transactions and dollar amount was higher in the unbanked population, and 90 per cent of unbanked Canadians are heavy cash users , illustrating that the unbanked are indeed turning to cash as their go-to payment method for their everyday purchases.

Virtual currencies - what is the hype?

Virtual currencies have been in a lot of news articles in recent years and have been a buzz word in the world of payments and beyond for a while. This is not an area of specific focus in our research, but we do continue to track it over time to understand if there are any major changes happening from year to year. Overall, only about five per cent of Canadians in our sample used virtual currencies to make a payment, averaging about seven payments and spending roughly $900. Awareness continues to increase, with about 97 per cent of Canadian consumers being aware of Bitcoin.9 So it is not likely that this payment instrument would become a significant substitute to cash in the near future. Interestingly, we find that younger Canadians and men are more likely to have made a payment using this instrument.

Conclusion

Overall, the innovations in electronic payments are providing Canadians with easier, faster, and more efficient ways to pay. Although historical trends suggest that cash and paper-based payments are indeed declining, Canadians are still using the same traditional payment methods. The question remains - Is Canada moving towards a cashless society? Our results suggest that cash and paper-based payments are still prevalent and will continue to be an important medium of exchange. Cash is easy to use and, more importantly, it is readily available and a convenient way to pay someone. For people who do not have a bank account, or don’t have a credit or a debit card, cash becomes their primary way of making payments.

As for cheques and money orders, using these payment instruments was more of an only given choice rather than a preference, especially in regions where cheques continue to hold their ground. The rise of electronic-based payment instruments will continue to grow, but there are always niche use cases for paper-based payment methods and cash that will be difficult to replace. Due to these reasons, we don’t believe that cash and cheques will become obsolete despite the rise of electronic-based payments and the benefits they bring.

Lastly, in order to provide the ultimate payment experience for Canadian consumers, Canadian institutions should innovate around those niche use cases of cash and cheques rather than stamp them out. The payment experience and the acceptance are the two most determining factors to the payment instruments Canadian consumers use. Thus, future generations of electronic payments should build around this concept and focus on improving the end user experience as well as the acceptance of the innovative payment instruments in order to remain competitive in the Canadian payment ecosystem.

What do you think about Canada moving towards a cashless society? We welcome and encourage readers to continue the dialogue in the comments below or to reach out to the authors directly.

Authors

Viktoria Galociova

Viktoria Galociova

As an Economist at Payments Canada, Viktoria is the lead author and researcher working on Payments Canada’s annual flagship publication: the Canadian Payment Methods and Trends report. Viktoria is also in charge of supporting the Modernization team, the Research team’s external blog and annual conference, as well as evaluating alternative data service options for the organization including supporting and contributing to the ecosystem surveillance function. Viktoria is also an active member of the Payments Canada Strategic Foresight Team. Viktoria’s recent work includes research on Canadian and international payment industry trends and international retail payment system research. Prior to joining Payments Canada, Viktoria conducted research relating to the economic impacts of oil prices, returns to higher education, the impact of socioeconomic factors on labour market outcomes and the impact of oil prices on housing markets. Viktoria holds a Master’s Degree in Financial Economics and a Bachelor’s Degree in Economics and Business from Carleton University.

Zheren Li

Zheren Li

As a Research Assistant for the Research unit at Payments Canada, Zheren supports the industry publication of the Canadian Payment Methods and Trends report. Zheren also contributes to long-term research of relevance to Payments Canada, prepares and presents findings of research to internal researchers. His research interests include applied statistics, generalized linear and nonlinear regression models, and theoretical analysis of methods used in research. Zheren holds a Bachelor’s degree in Psychology and he is pursuing a Master’s degree in Organizational Psychology at Carleton University.

[1] The data provided and discussed in this article is solely from the Payments Canada/Leger Marketing 2018 Canadian Consumer Payment and Transactions Survey. To read more about Leger Marketing, please click here.

[2] The survey asks for information on both point-of-sale (POS) and remote payments. Taking into account the ”recall factor”, thereby asking for the last seven days when it comes to POS payments while focusing on one month trends for remote payments (e.g. cheques) as these tend to be higher in value and conducted less frequently than POS payments (for e.g. bill payments).

[3] We also investigate the unbanked and underbanked in Canada. We define the unbanked as those individuals who do not have a credit or a debit card. The underbanked are those who either have a credit or a debit card, but not both.

[4] We do not include the other payment methods in this graph because they do not comprise of a significant amount of a person’s monthly spend.

[5] We define light users as those using a payment method for less than 25 per cent of their monthly spend, and 26 to 50 per cent as medium users, and heavy users are those individuals that spend over 50 per cent of their monthly spend with a particular payment method. These terms will be used throughout this article.

[6] Monthly cash totals are extrapolated from weekly volumes and values.

[7] In this article, we focus our analysis on using averages (means) rather than medians. We recognize that certain outliers may impact the averages but we believe that this provides an appropriate representation of the average Canadian’s payment habits.

[8] This segment is not very large, making up only about 4 per cent of our dataset but we find it is important to understand how they make payments as well.

[9] Bitcoin Sentiment Tracker by CorbinPartners and Payments Canada, available from: https://www.payments.ca/sites/default/files/2022-08/PaymentsCanada_2020BitcoinSentimentTracker_En.pdf

Disclaimer: The views presented in this paper are those of the authors and do not necessarily reflect the views of Payments Canada.