Changing the channel: mobile is taking over the online and offline point-of-sale

DISCLAIMER: Articles are written to reflect the interests and views of the author(s), and are not intended as an official Payments Canada statement or position.

Summary

The usage of mobile phones to make payments continues to rise in both the online and offline point-of-sale (POS).1 We expect this trend to accelerate with the introduction of open banking, ubiquitous digital ID and strong authentication, and the ever-expanding in-app and mobile experiences in the payments space. Big Tech and FinTech companies will also provide mobile-friendly banking and payments services for consumers, capitalizing on their predictive analytics.

In this paper, we provide an overview of the mobile experience in the online and offline POS context. We find that the convenience of mobile payments is starting to be embraced by consumers as they increasingly opt for mobile contactless and in-app payments. We also discuss demographics around mobile payment usage, and explore findings that consumers will increase their usage of mobile payments in the near future.

The mobile phone is becoming the interface of choice for making payments in Canada. We are seeing this happen across different environments, this includes the online and offline (or in-store) point-of-sale (POS) environments.2 A recent article finds that there are an estimated 6.8 million mobile payment users in Canada (a near fivefold increase since 2014).3 Ease of use and convenience are driving migration to the mobile interface (phones, tablets) in the payments industry and, with an addressable market of $605.9 billion in retail sales in Canada, there is a big opportunity for extensive growth.4 Much is expected of mobile payments over the coming decade.5 This shift will likely be driven by several converging factors.

First, open-banking will emerge in some form. This means at the least that vetted third-party application providers will be able to “read” and collate banking data. While “reading” is the current regulatory focus in open-banking6, in the future Canada may emulate European directives that allow some of these providers to “write” changes to payment users’ accounts - in other words initiate payments and transfers.7 This third-party application environment will provide the foundation to integrate Payments and banking with social networking using a mobile device. As is evident from WeChat Pay, AliPay, Venmo and other popular international payment apps, this convergence satisfies user needs and drives widespread adoption.

Second, digital identity solutions such as SecureKey’s Verified.me will facilitate remote payment account opening and management. At the same time, digital multi-factor authentication will allow secure payments to be made from those accounts, directly or through third-party apps. Big Tech and FinTech companies with clever algorithms are also beginning to provide mobile-friendly services traditionally offered by banks. This means that a number of services will increasingly be more intermingled with banking, offering users better products and services based on predictive analytics.8 As ID solutions emerge for other use cases beyond payments, such as age verification, driver licensing and health care, the physical wallet will be further supplanted by the phone, cementing it as the predominant conduit for payments.

As we stand on the cusp of a decade of profound change in payments, it’s helpful to examine current data and trends in mobile payments which can help serve as a benchmark for measuring coming change. We identified two environments: online and offline.

POS Payments: Online

The online POS environment includes transactions that take place in virtual merchant locations, including online store fronts and in-app e-commerce. For example, using the Starbucks app to order ahead or the Uber app to hail a ride. Many of these in-app payments leverage a card-on-file, which makes the payments experience invisible for consumers. In terms of card-on-file usage, younger consumers are significantly more likely to have their payment details saved in an app, with 57 per cent of 18-24 years olds having their payment information saved in- app (versus 26 per cent of the total).9 Among Canadians that have saved payment details in an app, the majority (almost 70 per cent) have a credit card as their default form of payment (debit cards are far away in second place at 14 per cent).10 When it comes to in-app payments, mobile phones are the go-to source and provide easy, speedy and convenient transactions. But what about the offline POS experience?

POS Payments: Offline (In-Store)

Offline POS payments or in-store payments, traditionally the domain of cash and card, are increasingly seeing the mobile experience interposition itself in the transaction. Physical credit and debit cards are starting to be left in the physical wallet and migrated to the mobile wallet. Apple Pay - first to market in late 2015 - is the most familiar and used mobile wallet.11

Uptake so far has been underwhelming as consumers scratch their heads over whether it’s easier to take a phone out of their pockets or a card. Among Canadians that are aware of mobile payments but have never made this type of transaction,, nearly half say “being happy with other payment methods” is one of reasons why they aren't using their mobile phone when they shop at brick and mortar stores.12 Contactless payments overall are particularly popular in Canada, and studies point to the two, card and mobile, being equally convenient, perhaps indicating why some Canadians have not made the transition.13 Of interest, once consumers have made the move, they seem to embrace it whenever possible. In fact, one in three Canadian mobile contactless payment users make mobile contactless payments whenever possible.14

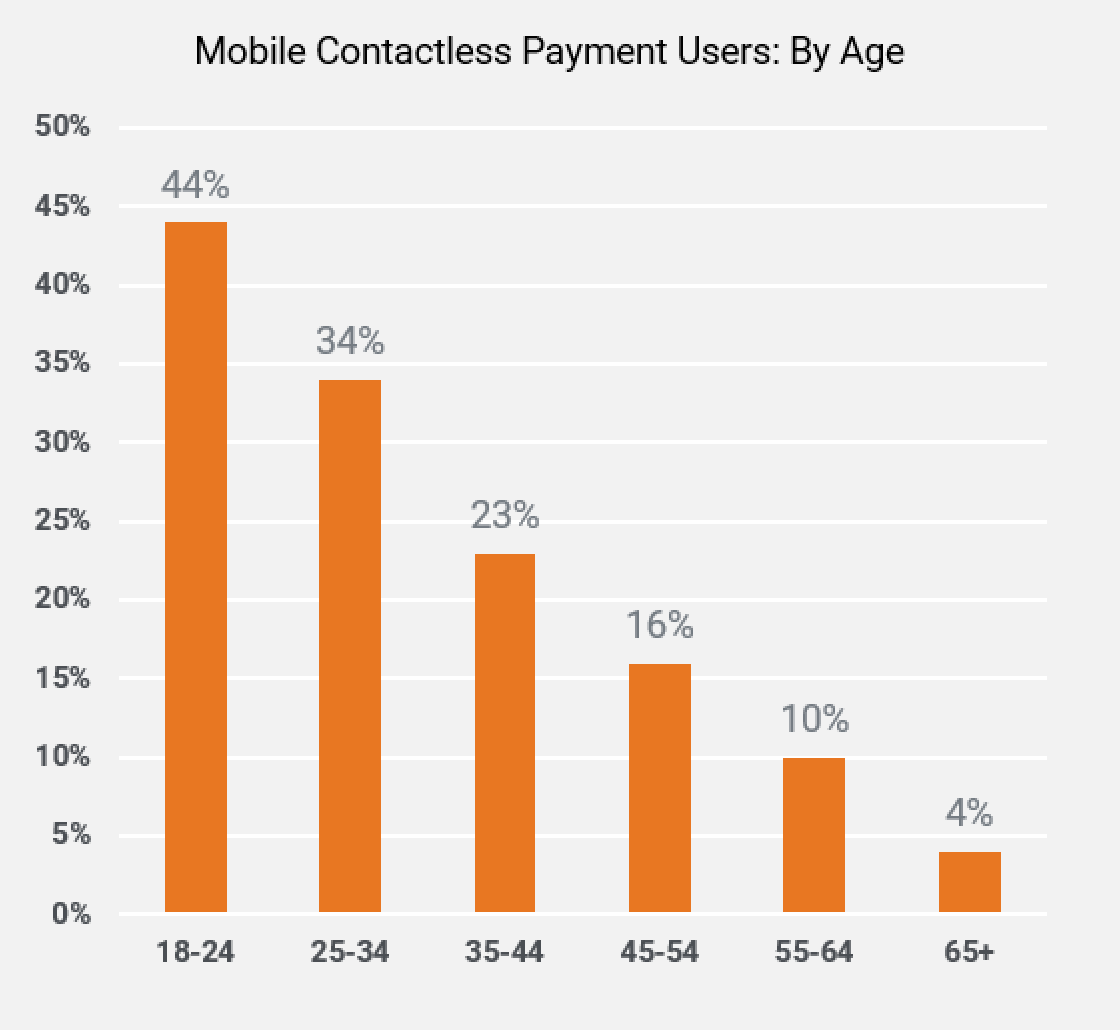

The use of mobile contactless payments differs by province and demographics. As expected, usage decreases with age. Of interest, residents of Alberta seem to be more inclined to use mobile contactless payments while Quebecers are more resistant (25 per cent vs 13 per cent, respectively).15

The use of mobile payments is also poised to climb higher: RFi Group finds that more than three in five mobile contactless payment users are planning on making more payments using their mobile device in the next 12 months. Even non-users are likely to migrate: Over one in four non-current users indicated that they would be likely to try making a mobile contactless payment if they were given the opportunity.16

How can we increase usage? Among existing users, the most common barriers preventing further usage are that customers can earn rewards by choosing other payment methods, as well as the difficulty confirming whether a merchant accepts this payment method or not. Among non-users, in addition to the lack of perceived need outlined above, security also continues to be a key barrier to migration with 34 per cent of non-current users mentioning it. This indicates there is a clear need for education and reassurance when it comes to newer methods of payment such as mobile contactless.

Innovation in the payments industry is increasing, providing more options for Canadians overall, and allowing them to pay with their mobile phone more seamlessly. As convenience and ease are further incorporated into payments, we believe there may be even faster migration away from “traditional” card payments. With this trend in mind, Payments Canada recently proposed a new rule that aims to enable a broader range of POS (offline or in-store) debit card acceptance. The key driver behind the creation of this rule is to accommodate the use of POS debit payments (both contactless and chip-and-PIN debit) for transit but also for other generally low-value purchases. As reasons for carrying a wallet fade with digital ID solutions being increasingly implemented or debit/credit card tapping payment options become available in public transit, mobile contactless is likely to grow. Beyond convenience, card numbers will be replaced with non-reusable temporary tokens during the transaction, increasing the overall security of the payment.

Authors

Viktoria Galociova

As an Economist at Payments Canada, Viktoria is the lead author and researcher working on Payments Canada’s annual flagship publication: the Canadian Payment Methods and Trends report. Viktoria is also in charge of supporting the Modernization team, the Research team’s external blog and annual conference, as well as evaluating alternative data service options for the organization including supporting and contributing to the ecosystem surveillance function. Viktoria is also an active member of the Payments Canada Strategic Foresight Team. Viktoria’s recent work includes research on Canadian and international payment industry trends and international retail payment system research. Prior to joining Payments Canada, Viktoria conducted research relating to the economic impacts of oil prices, returns to higher education, the impact of socioeconomic factors on labour market outcomes and the impact of oil prices on housing markets. Viktoria holds a Master’s Degree in Financial Economics and a Bachelor’s Degree in Economics and Business from Carleton University.

Jeffrey Stewart

As a Business Analyst at Payments Canada, Jeff is responsible for analyzing and developing educational material for the Canadian payments ecosystem and conducting research in support of payments modernization initiatives. His research interests include data in payments, closed-loop ecosystems, monetary policy and decentralized currency. Prior to joining Payments Canada, Jeff worked in the private and public sectors as a policy analyst, researcher and programmer, and as an independent business owner. Jeff holds Master's Degrees in Cognitive Science and Public Administration from Queen’s University.

1 The views presented in this paper are those of the authors and do not necessarily reflect the views of Payments Canada.

2 The point-of-sale (POS) environment includes transactions that take place in physical stores or via virtual merchant locations, including online store fronts and in-app commerce. POS payments methods include cash, prepaid, debit and credit card transactions. In 2018, POS payments accounted for almost 75 per cent of the total Canadian transaction volume, and nine per cent of the total transaction value. To read more please see the Canadian Payment Methods and Trends report.

3 To see more please see the following article.

4https://www.retailcouncil.org/wp-content/uploads/2018/08/Dec-RBTN_Oct_KSFinal.pdf

7 https://www.bofaml.com/en-us/content/psd2-regulation-aisp-pisp-payment-innovation.html

8 “Sale of recommended items, or items sold in addition to the main item, results in a thirty percent increase in Amazon’s sale yearly”. https://www.promptcloud.com/blog/how-amazon-focus-data-business-transformation/

9 RFi Group’s Canada Payments Council 2019.

10 Ibid.

11 https://www.emarketer.com/content/canada-mobile-payment-users-2019 / https://fortune.com/2016/06/01/apple-pay-expands-in-canada/

12 RFi Group’s Canada Payments Council 2019.

13 https://www.emarketer.com/content/canada-mobile-payment-users-2019

14 RFi Group’s Canada Payments Council 2019.

15 RFi Group’s Canada Payments Council 2019.

16 RFi Group’s Canada Payments Council 2019.