Cross-border payments: Canadian landscape and challenges

Introduction

Cross-border payments are financial transactions where the accounts of the payor and payee are based in different countries.1 Cross-border payments are typically more complex than domestic payments as they involve different national legal and regulatory frameworks, more than one currency, multiple time zones and often need to be facilitated through intermediaries and financial market infrastructures (FMIs).2 These transactions are essential to support international trade and economic activity, as well as in the movement of funds between people across the world.

However, these payments are not frictionless. The Financial Stability Board (FSB) has cited four challenges of cross-border payments globally:

- High costs;

- Low speed;

- Limited access; and

- Insufficient transparency.3

Depending on the jurisdiction, these challenges can have implications for economic growth, international trade, global development and financial inclusion. Additionally, this has impacts on the lives of consumers who seek to send or transmit payments internationally, whether this is sending remittances to friends and relatives in other countries, making payments when traveling or in the purchase of goods and services abroad.

Context

What are cross-border payments?

The FSB categorizes cross-border payments into three main segments: wholesale, retail and remittances.4

Wholesale

Wholesale cross-border payments represent the majority of cross-border transactions by value. They’re defined as payments between financial institutions (including banks and non-banks). Generally, these payments are used by financial institutions to support their own and their customers’ activities, including borrowing, lending, foreign exchange (FX) transactions, etc.5 These transactions are also used to conduct larger payments for the import and export of goods and services. Organizations that facilitate wholesale cross-border payment services include payment system operators, messaging networks, multi-currency settlement systems and commercial banks acting as intermediaries or correspondent banks.6

Retail

Retail cross-border payments are those between individuals and businesses. Typically, retail cross-border payments are low-value, high-volume transactions, representing the majority of cross-border transactions by volume. This sector includes cross-border traditional commerce and e-commerce, tourism, bill payments to providers abroad, electronic transfers and payments between individuals.

Key types of retail cross-border payments are: person-to-person (P2P), person-to-business (P2B), business-to-person (B2P), and business-to-business (B2B) (see Table 1). Major service providers include international card schemes, commercial banks and non-bank P2P payment providers such as payment service providers (PSPs).

Remittances

Remittance payments are a subsection of P2P retail payments. Remittances are primarily sent to receivers in emerging markets and developing economies. Major service providers include international money transfer operators, commercial banks, post offices (outside of Canada) and mobile money operators.

| Use case | Description |

|---|---|

| B2B | Payments for imports and exports of goods and services between businesses; including investments, revenue sharing, and intra-company payments. |

| B2P | Payments to individuals including marketplace payouts, claims and one-time disbursements, salaries and social benefits, and dividends and interest payments. |

| P2B | Payments from people to businesses, such as online e-commerce, verticals such as health or education, in-person travel/tourism, bill payments, loan repayments, and one-time payments and investments. |

| P2P | Payments between people in different countries, including remittances and account-to-account payments.7 |

Cross-currency transactions

An important distinction is between cross-border transactions that include cross-currency FX conversion and those that do not. In the case of the former, another party offers an FX conversion service. This means that they will exchange one currency for another to facilitate the transaction. Alternatively, cross-border transactions that do not require FX conversion (e.g., Eurozone) result in a change of the currency position of the payee and/or payor.8 In Canada, the majority of cross-border payments are also cross-currency transactions.

Why are cross-border payments important?

Cross-border payments are the method by which money moves between countries and, therefore, sit at the heart of international trade and economic activity. In 2020, North American cross-border payments represented USD$43 billion in revenue.9 Further, cross-border payments represent one-sixth of all transaction values globally, and is estimated to increase to over $250 trillion in value by 2027.10

Several factors have been attributed to this projected increase:

- Expanded supply chains across borders.11

- Increased asset management and global investment flows.12

- Growth in international electronic commerce (e-commerce).13, 14

- Increased remittance flows to low- and middle-income regions.15, 16

How do cross-border payments work?

Global cross-border payments are carried through a diverse multi-layered set of networks. These include more traditional arrangements, such as directly through a deposit taking institution. They may also occur through emerging arrangements, such as interlinkage of domestic payment systems, card networks, payment service providers (PSPs) and remittance services. Each arrangement can have different implications for the severity and type of challenges and risks encountered in the payment chain, such as the number of counterparties needed to complete compliance checks or the coordination of operating hours amongst payment systems.

Generally, there are two broad methods of settlement for cross-border payments; correspondent banking and digital currencies.

Correspondent banking

Correspondent banking is an agreement or contractual relationship between financial institutions to provide payment services on behalf of one another. This involves the opening of accounts by the respondent in the books of the correspondent for the provision of services. Correspondent banking is essential for customer payments and for the access of banks themselves to foreign financial systems and other international transactions.18 For example, a Canadian bank may establish a correspondent banking relationship with a bank in the United States, which would facilitate the exchange of currencies and access to the domestic payment system.17

Nearly all cross-border payments leverage correspondent banking relationships, including single platform and interlink solutions. Single platform — or closed loop arrangements — are PSP-run systems that connect the transacting parties, providing cross-border services to both payee and payor, such as Wise or PayPal. Alternatively, interlink arrangements constitute the integration of national payment system infrastructure to allow participants to send a payment directly cross-border to other participants. The link facilitates remote access to domestic systems or infrastructure for banks located abroad. These arrangements may differ in exchange and clearing, but will settle via networks of correspondent banks.

Correspondent banking utilizes the Swift network to transmit payment messages and instructions.19 Most cross-border payments that occur in Canada utilize the Swift network for message exchange and payment instructions.

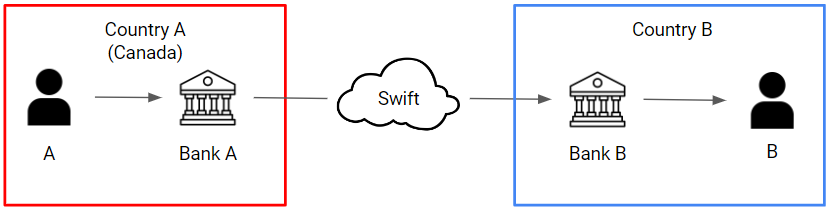

Below is an example of a cross-border correspondent banking transaction flow. This flow assumes that Bank A holds a nostro20 account at Bank B, meaning they possess an account that contains the currency of the country in which Bank B is located. Consider an individual (A) in Canada, who banks at Bank A, that wishes to send money in USD to an individual (B) in the United States who banks with Bank B. If Bank A holds a USD account at Bank B, then this represents the transaction flow.

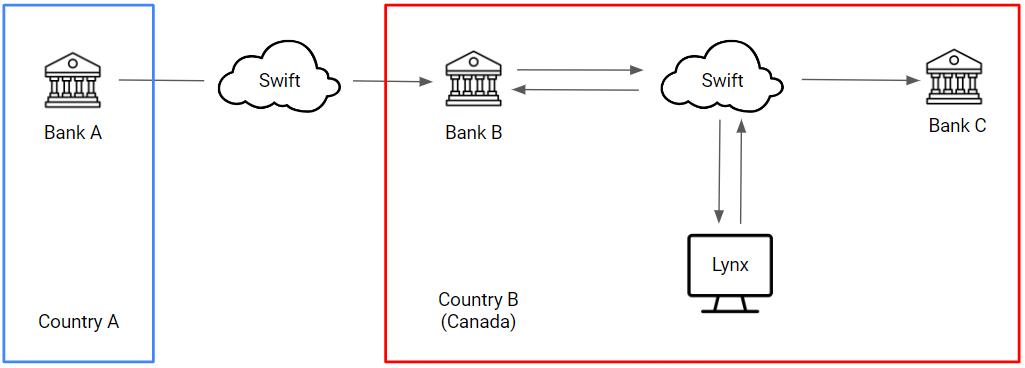

The figure below illustrates transactions that will utilize Lynx for interbank transactions when they are denominated in Canadian dollars (CAD), or to complete a CAD-denominated payment for institutions that do not possess correspondent banking relationships. This transaction flow assumes that Bank A maintains a correspondent banking relationship with Bank B, meaning that they possess a nostro account at Bank B. However, the funds, ultimately, need to reach Bank C. Both Bank B and C are participants in Lynx.21 Therefore, Bank A can transact with Bank B, and Bank B can transfer the funds to Bank C via a Lynx payment. This transaction will be completed in Canadian dollars.

Digital currencies

Settlement of cross-border payments using digital currencies leverages arrangements that use decentralized infrastructures to eliminate intermediaries between payor and payee, which is primarily through cryptocurrencies.22 Cross-border payments can be made on distributed ledger networks for the direct transfer of crypto funds.23

While less common, payments can be made cross-border using digital assets that do not rely on correspondent banking and instead utilize an online ledger. Crypto assets and currencies, including stablecoins, can be exchanged peer-to-peer between two accounts in an online ledger and then sold for fiat currency. It is for this reason that peer-to-peer cross-border payments do not use correspondent banks in the management of an online ledger.

Challenges

G20 Roadmap for Enhancing Cross-border Payments

The FSB has been leading work to assess and address the four challenges identified in cross-border payments from an international perspective. At the request of the G20, the FSB has developed a roadmap to enhance cross-border payments in coordination with the Committee on Payments and Market Infrastructures (CPMI) and other relevant international organizations and standard-setting bodies.

The Roadmap for Enhancing Cross-border Payments (Roadmap) has been endorsed by the G20 leaders and provides a high-level plan.24 Two foundational steps in the Roadmap were the setting of quantitative global targets using key performance indicators (KPIs) to address the four challenges endorsed by the G20 leaders and the development of three interconnected priority themes. Most recently, data has been collected in KPI monitoring reports, and while more data is required to understand the current state across jurisdictions, practical projects have been established to achieve the G20 targets.25

Challenges in cross-border payments

As detailed by the FSB, the major challenges present in cross-border payments internationally are high cost, low speed, limited access and insufficient transparency:

- High cost consists of various elements, including transaction fees, account fees, compliance costs, applied FX conversion rates and fees and liquidity costs for prefunding.26 Further, the number of intermediaries involved can compound costs.27

- Low speed involves the processing time of a payment from end-to-end, including factors such as the time required for reconciliations, processes for funding and defunding, daily cut-off and closing time and Anti-Money Laundering/Know Your Client (AML/KYC) checks.28 This can impact business operations, cause organizations to experience cash flow burdens and negatively affect end- users/consumers.

- Limited access includes limitations for users in accessing services and for PSPs in accessing payment systems and other arrangements. This has important implications for financial inclusion for individuals and businesses.

- Insufficient transparency refers to the availability of information about costs, speed, processing chains and payment status, which presents challenges for end-users and service providers. Intermediaries involved in the process may possess different practices, legal requirements and messaging standards, which can create difficulties for entities to track payments and obtain a clear picture of the costs, movements and deductions involved.

Canadian landscape and opportunity

Based on Canadian data and findings, the most significant challenges for Canadians appears to lie in the high cost and slow speed of retail and remittance cross-border payments. While there are areas of concern for wholesale Canadian cross-border payments, they appear to be less significant in the Canadian context.

Costs appear to be of particular concern in the retail and remittance space; however, cited to be high and variable based on the transaction value. For example, some providers will apply fees based on a percentage of the transfer value, or may alternatively apply a fixed fee for the transaction. As such, costs will vary significantly based on the provider and the value of the Canadian businesses and consumers have stated that lower value international payments, including remittances, are often more expensive than higher value retail transactions. Remittance prices, specifically, are higher in Canada than in comparable jurisdictions.

The speed of these payments is also highly variable, particularly for those sending retail and remittance transactions. Some providers will offer funds availability within 30 seconds, whereas others can take up to two business days, depending on the currency. Canadians have stated that the time required for money to appear in beneficiaries accounts is too long. While data is lacking in the Canadian context, these challenges in retail and remittance transactions appear related to technological shortcomings, standards differences, time zones and payment system accessibility and compliance concerns (including AML/KYC) across jurisdictions.

One area in which Canada appears to be performing well is in access to cross-border payment services. Canada has a low percentage of unbanked and underbanked Canadians, roughly one and ten percent respectively.29 Further, most end-users have multiple options when considering retail and remittance accessibility, including banks (P2B, B2B, B2P), international card schemes (P2B, P2P) and other service providers (P2P).30

However, another facet of access relates to the ability to participate in national clearing and settlement systems. PSPs in Canada do not currently have direct access to payment systems, including those owned and operated by Payments Canada. Currently, in conjunction with industry, Payments Canada is advocating for amendments to the Canadian Payments Act to expand membership eligibility to include PSPs, alongside other financial entities. This legislative amendment would improve accessibility of payment systems and related arrangements for PSPs in Canada.

Finally, transparency is also an area in which more Canadian data is needed. Opacity has been noted in the wholesale space, with costs, rates and fees sometimes being unclear or unknown. Canadian businesses have also demonstrated that unknown exchange rates and confirmation of payment are key pain points — particularly among online providers — for international payments.31

Payments Canada’s systems

Payments Canada is guided by its mandate outlined in the Canadian Payments Act (CP Act) to establish and operate national systems for the clearing and settlement of payments; facilitate the interaction of its clearing and settlement systems with other systems; and facilitate the development of new payment methods and technologies. In pursuing this mandate, Payments Canada is required to promote the public policy objectives of efficiency, safety and soundness of its clearing and settlement systems and taking into account the interests of users.

Currently, Payments Canada does not assume an active role in Canadian cross-border payments, acting only to ensure its systems support the settlement of the domestic side of some cross-border payments. The organization does not have any rules or operations for facilitating cross-border payments, directly, but does clear and settle the Canadian dollar leg of cross-border payments in Canada. However, the organization has embarked upon modernization efforts, including the introduction of ISO 20022-capable systems, intended to create a common language for payments internationally. The payment and cash management messages were developed with consideration of cross-border payment guidelines and rules, defining how these messages should be used to execute cross-border payments and the reporting of cash transactions to provide enhanced and more structured data.

Conclusion

Cross-border payments are complex, and the challenges and necessary data require more thorough exploration, including in the Canadian space. More Canadian data is needed to better understand the specific challenges in Canadian cross-border payments.

Payments Canada is investigating the challenges in the Canadian cross-border space as it relates to the functionality of its systems and within the bounds of its mandate. Furthermore, Payments Canada is advocating for expanded access to its payment systems to include PSPs, credit union locals and the operators of designated financial market infrastructures, which may improve access metrics for Canadian cross-border payments.

1 Bank of England. Cross-border payments. January 31 2023.

2 Financial Market Infrastructures are systems that facilitate the clearing, settlement, or recording of payments, securities, derivatives, or other financial transactions among participating entities.

3 Financial Stability Board. G20 Roadmap for Enhancing Cross-border payments: Priority actions for achieving the G20 targets. February 23 2023.

4 Financial Stability Board. Targets for Addressing the Four Challenges of Cross-Border Payments. October 13 2021. http://www.g20.utoronto.ca/2021/FSB-Targets-for-cross-border-payments-roadmap.pdf

5 Ibid.

6 Ibid.

7 Visa. Let’s give a voice to end-users: Cross-border payments, attributes, and use cases. January 2023.

8 European Central Bank. Towards the holy grail of cross-border payments. August 2022.

9 Drawn from internal data.

10 McKinsey & Company. A vision for the future of cross-border payments. October 2018.

11 Bank of England. Cross-border payments. January 31 2023.

12 RBC Wealth Management. Shaping tomorrow, today: The next generation of global enterprising families. 2020.

13 Terzy, N. The impact of e-commerce on international trade and employment. October 25, 2011.

14 heyworld. North America Cross-Border eCommerce Insights and Facts. 2022.

15 Dimbuene, Z. T. & Turcotte, M. Statistics Canada. Study on International Money Transfers from Canada. April 17, 2019.

16 Ibid.

17 Financial Stability Board. Enhancing Cross-border Payments: Stage 1 report to the G20. April 9, 2020.

18 Bank for International Settlements. Committee on Payments and Market Infrastructures: Correspondent Banking. July 2016.

19 Swift is the leading provider of secure financial messaging services.

20 Nostro and vostro terminology is used to differentiate between accounting records held by banks. Nostro refers to ‘our’ money at another bank, whereas vostro refers to ‘your’ money on deposit at ‘our’ bank.

21 Lynx is Canada’s high-value payment system, owned and operated by Payments Canada.

22 Reserve Bank of Australia. Digital Currencies. 2022.

23 Adrian, T. & Mancini-Griffoli, T. International Monetary Fund. Technology Behind Crypto Can Also Improve Payments, Providing a Public Good. February 23, 2023.

24 Financial Stability Board. Enhancing Cross-border Payments: Stage 3 roadmap. October 13, 2020.

25 Financial Stability Board. G20 Roadmap for Enhancing Cross-border Payments. October 9, 2023.

26 Financial Stability Board. Targets for Addressing the Four Challenges of Cross-Border Payments. May 31, 2021.

27 Ibid.

28 Ibid.

29 Payments Canada. Rebound and Grow: Canadian Payment Methods and Trends Report 2022. 2022.

30 Financial Stability Board. Targets for Addressing the Four Challenges of Cross-Border Payments. May 31, 2021.

31 Drawn from internal data.

Author

Gillian Monckton

Gillian Monckton is an Analyst at Payments Canada on the Lynx and Emerging Policy Team supporting various policy projects on both the emerging policy side and related to Payments Canada’s systems. Gillian completed her Master of Public Policy at the Munk School (University of Toronto), where she specialized in economic policy. Her passions are related to financial inclusion in payments, access to national payment systems, payment innovation and emerging payments, and cross-border solutions.