Canada reaches $11.7 trillion in payment transactions in 2022 – up seven per cent in value from 2021

Credit card use grew 30 per cent while cash use declined 41 per cent over last five years, Payments Canada study reveals.

Key study highlights:

- While total payment volume declined two per cent compared to five years ago, total payment value increased by 21 per cent.

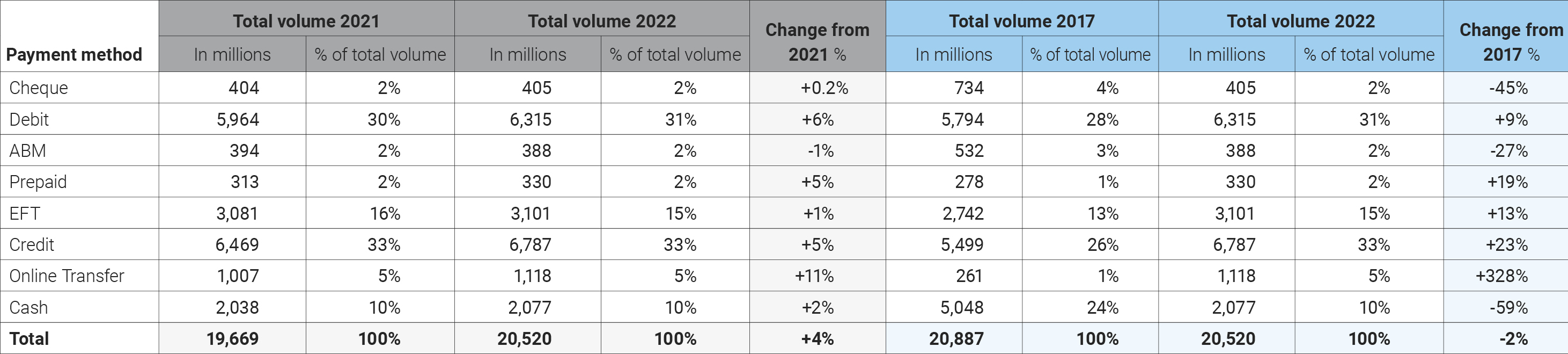

- Credit cards represent 33 per cent of payment volume in 2022, followed by debit cards (31 per cent); electronic funds transfer (15 per cent); cash (10 per cent); online transfer (five per cent); cheque, automated banking machine (ABM) and prepaid cards (all at two per cent).

- Cash use recovered to pre-pandemic levels, with one in 10 transactions paid in cash in 2022.

- Almost nine in 10 (89 per cent) Canadians tapped a payment card at least once a month for a store purchase in 2022.

- For the first time, online transfer payments surpassed personal EFT (electronic funds transfer) based on volume.

- 1.06 billion e-transfers were sent in 2022, up 11 per cent in volume from 2021.

- Nearly half (48 per cent) of existing buy now, pay later (BNPL) users increased usage in 2022.

- While 49 per cent of Canadians are aware of cryptocurrencies, only 14 per cent have used cryptocurrency, primarily as an investment rather than for payment purposes.

OTTAWA, October 5, 2023 – Today, Payments Canada released its annual Canadian Payment Methods and Trends 2023 report, which analyzes 20.5 billion payment transactions made in 2022 totaling $11.7 trillion (more than $475 billion every business day) and highlights the trends shaping the Canadian payment landscape.

Year-over-year trends: Credit and debit cards continue to be the top two payment methods

- Transaction volumes and values across all payment types, with the exception of cheques, experienced year-over-year growth in 2022.

- Credit cards represented 33 per cent of all payment volumes in 2022, followed by debit cards (31 per cent); electronic funds transfer (15 per cent); cash (10 per cent); online transfer (five per cent); cheque (two per cent); ABM (two per cent); prepaid cards (two per cent).

- Electronic funds transfer represented 59 per cent of total payment value in 2022, followed by cheques (28 per cent); credit cards (six per cent); debit cards and online transfers (both three per cent); ABM (one per cent); cash (0.5 per cent); prepaid cards (0.2 per cent).

- Online transfer continued to be the fastest-growing payment type with year-over-year volume growth of 11 per cent and value growth of 19 per cent from 2021. Interac e-Transfer continued to dominate the online transfer payment segment with more than three in five Canadians (61 per cent) using Interac e-Transfer to either send or receive a payment in a given month.

- Credit card volume increased five per cent, while debit card volume increased six per cent year-over-year in 2022 compared to 2021.

- The average credit card transaction value was $99, while the average debit card transaction value was $47.

- Cash use grew two per cent in volume, with the average cash transaction value at $29.

Five-year trends: Online transfer continued to be the fastest-growing payment type

While total payment volume declined by two per cent compared to five years ago, total payment value increased by 21 per cent during this same period.

- While online transfers represent a small portion of total payment volume, they experienced the highest growth of any payment method over the past five years (328 per cent in payment volume and 314 per cent in payment value) and are poised to overtake cash.

- Within the card space, credit and prepaid cards lead the way in terms of volume growth at 23 per cent and 19 per cent respectively.

- Debit card volume increased by nine per cent.

- Cash and cheque transaction volumes decreased by 59 per cent and 45 per cent.

“We have seen a dramatic shift towards digital payment options over the past five years. Evolving technologies will continue to influence how Canadians make and receive payments,” said Tracey Black, President and CEO of Payments Canada. “Payments Canada continues to work collaboratively with the payment ecosystem to provide Canadians and Canadian businesses with convenient, safe and efficient payment options.”

One-year and five-year Canadian payment transaction volume trends

One-year and five-year Canadian payment transaction value trends

Evolving payment innovations and future outlook

Canadians are increasingly comfortable using digital payments and are embracing frictionless payment experience as the number of digital payment options continues to grow.

- Although cash use has declined over the past five years, cash will still be used as a store of value and means of payment. Close to half of all consumers (49 per cent) and businesses (46 per cent) in Canada believe that retail outlets will be completely cashless in the next ten years. Yet, two out of five consumers and businesses (45 per cent and 41 per cent, respectively) would feel uncomfortable if they could not use cash for making purchases.

- Credit card usage is well positioned to grow as Canadians continue to embrace mobile payments at the point-of-sale and mobile commerce. In 2022, 57 per cent of mobile wallet users in Canada reported using their credit card(s) linked to their mobile wallet for their purchases.

- Prepaid cards are expected to experience the highest growth in both volume and value over the next few years compared to all other payment cards. Prepaid card usage increased among Canadian youth (14-18 years) as parents leveraged open-loop cards to provide an allowance and to track spending, in addition to international students spending money received from home. Innovation will continue to transform the prepaid card space with solutions ranging from remittance cards and gift cards to cryptocurrency payments.

- Thinking about the future of digital payments, 65 per cent of Canadians would send their payments in real-time if the option was available. The top three use cases for sending payments in real-time are paying a credit card bill, government taxes and rent.

“In 2022, Payments Canada published ISO 20022 messages for Lynx and the upcoming Real-Time Rail (RTR). The ISO 20022 message standard supports data-rich payments - more information about the payment traveling with the payment. ISO 20022 will support enhanced and new payment experiences for Canadian businesses and consumers. Payments Canada will continue to drive innovation to ensure payments are easier, smarter and safer for all Canadians.”

About the study

Payments Canada worked closely with payment service providers, payment consultants and researchers to compile a comprehensive 2022 data set and provide insights into how Canadian consumers and businesses pay. The general methodology involves a combination of industry data and market research. Industry data is derived primarily from the Automated Clearing Settlement System (ACSS) data, industry payment card usage data and quantitative and qualitative market research sources. Data is also collected from payment service providers and payment networks on an aggregated annual basis, based on actual payment instrument usage data. Survey research is used to fill data gaps and provide detailed insights.

About Payments Canada

Payments Canada is a public purpose organization that owns and operates Canada's payment systems, Lynx and the Automated Clearing Settlement System (ACSS). Payments Canada is responsible for the physical infrastructure and the associated by-laws, rules, and standards that support these systems. It also has a duty to promote the efficiency, safety, and soundness of Canada's payment systems while taking into account the interests of end users. In 2022, Payments Canada's systems cleared and settled over $119 trillion—more than $476 billion every business day. Transactions that pass through these systems include debit card payments, pre-authorized debits, direct deposits, bill payments, wire payments and cheques initiated and received by Canadians and Canadian businesses. Payments Canada is working closely with the payment ecosystem to modernize Canada's payment systems to ensure Canada and Canadian businesses remain globally competitive.

For media inquiries, please visit our media centre.